Business Plans - Comprehensive Guide Part 6

A comprehensive Business Plan should include essential financial and strategic elements to ensure thorough planning and analysis. A cash flow statement tracks the inflows and outflows of cash, while the profit and loss statement details revenue and expenses to determine profitability. The cost of goods sold (COGS) is crucial for understanding direct production costs, and the balance sheet provides a snapshot of the company's financial position. Contingency and "what if" plans prepare the business for potential uncertainties, and appendices offer supplementary information and detailed data. Regular business plan reviewing ensures the document remains relevant and responsive to changing conditions, guiding the business toward sustained success.

1. Measuring financial performance

There are three financial statements a business uses to measure their financial performance:

a. Cashflow Statement

b. Profit and loss statement

c. Balance sheet

a. Cashflow Statement

Cashflow is a pinnacle part of a business, if there are serious concerns it is vital that you gain help asap, talk to your bank and accountant.

The Cashflow statement summarises the current incoming (revenue) and outgoing (expenses) figures and provides a snapshot of the business’s current status over a given period of time, helping to manage the business.

Reviewing bank statements can help with compiling the figures.

Include:

- Sales receipts - records of transactions at the point of sale

- Cash receipts - revenue received

- Credit receipts - revenue refunded

- Accounts receivable - revenue pending receipt

- Accounts payable - revenue payments to be made by the business

- Wages - internal and external

- Expenses for marketing and advertising events. There are always expenses if you are having an event, so don’t forget to add them

- Expenses for small items, like a labelling machine or decorations for the office, can quickly add up and surprisingly often can break a business’s budgets

- Interest on loans and bank charges and fees can pile up before you know it

- Build in an ample amount, under ‘Miscellaneous costs’, for unexpected and unforeseen expenses

b. Profit and Loss Statement

Also known as an Income statement. Information is taken from the Sales Forecast; expenses budget and the Cash Flow Statement. The income statement tracks and predicts the profit or loss of a business in a given period by comparing revenue to expenses.

Provide details for the year as well as figures for the next three years.

Calculating profit or loss:

X Total revenue for the month

Y Total of all expenses for the month

X minus Y = the business profit or loss

c. COGS (Cost of Sales and Cost of Goods Sold)

Cost of goods sold (COGS) and Cost of sales both measure business expenses to produce a product or service.

It is essential for a business to understand the true cost of making a product or providing a service to its customers to ensure competitive and profitable mark-up.

Small business owners who start out working from their home for production and warehouse purposes see a massive change when they progress to dedicated manufacturing or warehousing premises resulting in their COGS dramatically increasing.

Monitoring COGS helps business owners identify and address the areas that can put pressure on their profit margins.

As service-only businesses do not produce a physical item, therefore cannot calculate operating expenses so uses the Cost of Sales or Cost of Revenue.

In a manufacturing business COGS includes all the direct costs necessary to produce a finished product. Materials and parts are not the only costs incurred to manufacture a product.

Direct costs

- Raw material costs or items for resale

- Cost of inventory of the finished products

- Supplies to produce the products

- Packaging costs and work in process

- Supplies for production

- Overhead costs, including utilities and rent

- Labour involved in the production

- Lease and energy costs for dedicated workshops or factories

Indirect costs

Any costs that do not relate directly to the manufacture of the product are to be excluded, e.g. Distribution, marketing and general admin.

- Labour, the people who put the product together

- The equipment used to manufacture the product

- Depreciation costs of the equipment

- Costs to store the products

- Any back-office costs related to the production of the product

COGS formula

(Beginning Inventory + Purchases) – Ending Inventory = COGS

COGS example

The company has the following information for recording the inventory for the calendar year ending on December 31, 2023.

Recorded on January 1, 2024,the inventory is £20,000.

On December 31, 2023,the ending inventory is £6,000.

During the year, the business made £8,000 worth of purchases.

COGS = (£20,000 + £8,000) - £6,000

COGS = £22,000

This information lets you calculate the true cost of goods sold in the calendar year. COGS helps you to evaluate the cost and profits but also helps plan out purchases for the next year.

Gross margin and gross profit

- Subtract COGS from sales.

The higher your COGS, the lower your margins will be; therefore, it is imperative that you regularly monitor your cash flow.

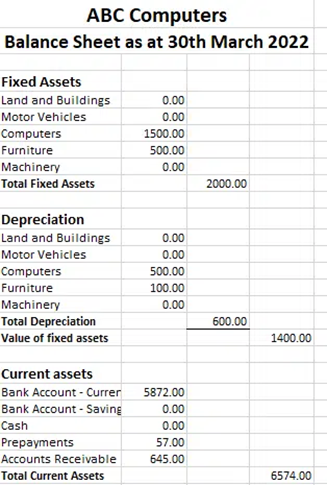

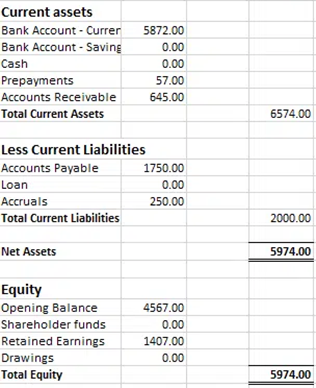

d. Balance Sheet

A Balance Sheet is an accounting report and is required by all companies registered at Companies House and very helpful for self-employed to see their financial health.

It shows the net worth of a company by comparing your:

i. Assets (what you own)

ii. Liabilities (what you owe)

iii. Equity (the net difference when you subtract liabilities from assets)

Example Balance Sheet:

i. Assets (what you own)

Assets represent:

- The cash in the business

- The value of the equipment

- Inventory

- Accounts receivable (money that is owed to the company)

Assets can be split into three sections:

- Current assets

- Intangible assets

- Fixed assets

Current Assets

Current assets are those that can be converted into cash within a year. These include money in the business bank account, inventory on hand, and accounts receivable (money owed by customers).

Inventory encompasses anything a business owns with the intention to sell, including products currently in stock.

Intangible Assets

Intangible assets, such as Intellectual Property Rights (IPR), cannot be seen or touched but hold significant value. These assets are recorded on the balance sheet when purchased.

Copyrights

Check that no-one else has already had your idea and it is tangible and commercially viable, then you should protect it.

Items which are automatically copyrighted:

- original literary, dramatic, musical and artistic work, including illustration and photography

- original non-literary written work, eg software, web content and databases

- sound and music recordings

- film and television recordings

- broadcasts

- the layout of published editions of written, dramatic and musical works

The copyright holder has the exclusive rights to publish, copy, distribute and sell their creation and no one else can use their work without their permission.

The distinguishing design, the shape and form of an object, is protected.

You will still receive the full level of copyright protection whether you use the official symbol or not, ©, but this is only for unregistered copyright in the UK.

For own designs copyright protection lasts for 10 years from the minute it was sold or 15 years from the moment of creation, whichever comes first.

You can provide a licence for others to use it, this is a contractual agreement whereby the owner of the copyright states the ways the work can be used, whether it can be changed and any costs to be incurred.

The copyright can be sold, usually via a contract.

Patents

Frequently Patents are used to protect inventions. A patent gives the holder the right to take legal action against anyone, without their permission, to use or sell your inventions. The invention must be new and not a modification to receive a Patent. Before you apply for a Patent, it is important to thoroughly check no one else has registered it.

It may be beneficial to get specialist help with the application process as it can be complicated and expensive.

Trademarks

To register a trademark your brand must be unique. If you want to protect the visual identity (brand) of your product or service then a Trademark is needed. Legal action can be taken against anyone who copies your brand without your permission.

Items that can be trademarked within your brand:

- Words

- Sounds

- Colour schemes

- Logos

Misleading words or offensive terms or images cannot be trademarked.

You can show your brand is trademarked by using this symbol next to your brand name, ®.

Fixed Assets

Fixed assets, or long-term assets, are items that the business owns and intends to use for an extended period. These include premises, equipment, land, and vehicles.

The purchase of a fixed asset is recorded on the balance sheet.

The cost of the asset is called ‘The original cost’. Over time, the asset depreciates in value and this must be reflected in the balance sheet.

ii. Liabilities (What is owed)

Liabilities are future payments that a company is obligated to pay.

Business liabilities include business loans, taxes, hire purchase, rent and money owed to suppliers.

Current liabilities

It is common for most businesses to have several current liabilities, deferred revenue e.g. accounts, taxes and wages payable.

It is essential to monitor your current liabilities, if they get too high your business could fall into financial trouble.

Long-term liabilities

Long-term liabilities are financial obligations or debts that are due to be paid over a period greater than a year.

Included is loan and lease payment and money owed on a mortgage.

iii. Equity (the net difference when you subtract liabilities from assets)

Equity is the net difference when you subtract Liabilities from Assets.

Owner’s and Shareholder equity, shows the proportion of the business that belongs to its owners and/or shareholders.

When a profit is made, the amount is added to the owners’ and/or shareholders’ equity. When losses are incurred, the amount is subtracted from owners’ and/or shareholders’ equity.

2. Risks and threats

a. Risk Assessment

Before a business can put together a Contingency Plan it needs to carry out a thorough Risk Assessment.

A Risk Assessment identifies internal and external risks, evaluates their likelihood and potential impact, and recommends mitigation actions. Risk analysis can uncover issues in requirements, manage software and hardware defects, and address other potential problems.

- Complete the Risk Analysis model – see template below

Risk Assessment template - https://www.hse.gov.uk/simple-...

|

What are the hazards? |

Who might be harmed and how? |

What is already being done to control the risks? |

What further action is needed to take control of the risks? |

Who needs to carry out the action? |

When is the action needed by? |

Done |

b. Contingency Plan

Once a Risk Assessment has identified potential risks and a plan in place to develop strategies to mitigate their negative impact a Contingency Plan can be created.

Often referred to as Backup Plans or Plan B, Contingency Plans are designed for exceptional risks that could have catastrophic consequences. These Plans are crucial for addressing risks that could affect a project's timeline, budget, or quality, helping businesses and projects across various industries maintain resilience and stability.

Analyse the results the implement the necessary steps you would take in a worst-case scenario that could have a detrimental effect on your Business.

Whether it be losing a key member of your management team, a loss of market share or heavy pressure from the competition, your Business needs to be able to proactively and strategically react to avoid a crisis.

When seeking funding a Contingency Plan will often be required and demonstrates that you have considered unusual circumstances such as a huge loss of market share.

BASIC CONTINGENCY PLAN

|

BUSINESS IMPACT ANALYSIS

|

During this phase, you will evaluate potential impacts that could negatively affect your business operations and create a Business Impact Analysis (BIA). The BIA will identify critical business functions, assess the consequences of disruptions, and estimate recovery times. Once the BIA is completed, review it with senior management and key stakeholders to ensure they understand the findings and the importance of visibility. This collaborative review process will help align the organization's response strategies and ensure all parties are informed and prepared to address potential risks effectively. |

||

|

RECOVERY STRATEGIES

|

Identify and document all resource requirements from the Business Impact Analyses (BIAs), including personnel, equipment, facilities, technology, and finances. Develop and document a recovery strategy tailored to these needs, covering short-term and long-term actions. Implement the strategy, ensuring all staff are trained and aware of their roles. Regularly review and update the strategies to adapt to changes in the business environment or operational requirements. |

||

|

PLAN DEVELOPMENT

|

Develop a comprehensive framework for the contingency plan by establishing and organizing recovery teams with clearly defined roles. Create a detailed relocation plan to ensure smooth operation in case of disruptions. Develop thorough Business Contingency (BCP) and IT Disaster Recovery Plans (IT DRP), documenting all procedures, resource requirements, and contact information in a flexible, easily updated document. Ensure this document is regularly reviewed and accessible to all relevant stakeholders. Finally, seek approval from upper management to ensure support and integration of the plans into the organization's operational framework. |

||

|

TESTING & EXERCISES

|

Develop a test plan with exercises to validate the Business Contingency Plan (BCP). Conduct regular drills and table top exercises to simulate various disruption scenarios, involving all relevant personnel. After each exercise, review performance and gather feedback. Update the BCP based on test results to address any weaknesses or gaps. Regularly revise and communicate updates to ensure the plan remains effective and the business is well-prepared for disruptions. |

c. The What-If Plan

The What-If Plan, or Scenario Analysis, can be used when a business decision is being considered that would pose a risk to the business, for e.g. seeking funding, looking to expand, increase the workforce or making an acquisition.

A Contingency Plan and a What-If Plan both prepare for unexpected events, but they serve different purposes and scopes:

Contingency Plan:

- Purpose: Provides a structured response to specific, anticipated disruptions.

- Scope: Covers broad, significant risks with detailed procedures.

- Components: Includes predefined actions, roles, resources, and recovery strategies.

- Use Case: Activated during major incidents like natural disasters, system failures, or significant operational disruptions.

What-If Plan:

- Purpose: Explores potential scenarios and their outcomes to develop flexible responses.

- Scope: Addresses a wide range of hypothetical situations, often less severe.

- Components: Focuses on analysis and brainstorming, with multiple possible actions for various scenarios.

- Use Case: Used for planning around minor disruptions, market changes, or new business opportunities.

In essence, a contingency plan is a specific, actionable strategy for known risks, while a what-if plan is a more flexible approach for a variety of potential scenarios. Both are crucial for comprehensive risk management.

3. Appendices

Whilst your primary Business Plan should be concise and uncomplicated, there may be information you choose not to include in the body of the plan itself but you still want people able to refer to.

Reference the relevant appendices in the body of your Business Plan.

Example appendices:

- Graphs, tables and notes

- Market research data that verifies your claims

- Detailed financial forecasts and assumptions

- CVs of key personnel (essential if you are seeking outside funding)

- Product literature or technical specifications

4. Business Plan reviewing

Your Business Plan is a living document and should be referred to frequently to re-evaluate your vision, check that you are on track and hitting your goals and fully utilising the brilliant ideas you had at the beginning.

Review whenever something changes:

- Account changes

- Developments within your industry and business

- Branching into a new market sector

- Release of new product

- Taking on a business partner

- Seeking funding

- Manage rapid growth

- Moving premises

A comprehensive Business Plan that includes a cash flow statement, profit and loss statement, cost of goods sold (COGS), balance sheet, contingency and "what if" plans, appendices, and regular business plan reviews is essential for effective financial management and strategic planning. These components collectively provide a detailed understanding of the company's financial health, operational costs, and overall performance. Contingency plans ensure preparedness for uncertainties, while appendices support data transparency. Regularly reviewing and updating the business plan ensures it remains aligned with current market conditions and business goals, fostering sustained growth and success.

To view the other articles in this series follow this link: https://bespokeuk.com/post-cat...

2026 Colours trends for website design

2026 Colour Trends for Website Design Digital spaces are undergoing a prof...

8 min read

Google analytics dropping?

1. Google Analytics The old version of Google Analytics (known as Universa...

5 min read

Stop business subscriptions with Bespoke software

Subscription Creep: hidden system costs Many business owners genuinely bel...

7 min read

E-commerce Design strategies for 2026 success

Ecommerce Design strategies for 2026 Success To achieve Ecommerce success...

4 min read

Business sustainability - Understanding Carbon Footprint, Carbon Neutral, and Net Zero

The concepts of carbon footprint, carbon neutrality, and net zero are centr...

9 min read

The cost of manual, repetitive admin tasks

Human Error and Wasted Hours In countless small and medium sized businesse...

4 min read